-

Home

-

International Report

- The Americas

The Americas

Is SLOW the operative term for brewing behemoths? It has taken MillerCoors, the number two brewer in the U.S., a full two years to answer Bud Light Platinum with its own more alcoholorific line extension called Miller Fortune. Miller Fortune’s alcohol content is to be a bit higher than its competitor’s, although both are aimed at "millennial males" (those born after 1980) and hope to steal share from fast-growing liquor brands.

The Americas

Sometimes obstinacy will be rewarded. That’s why SABMiller has decided to take its case against the exclusive sales agreement between Mexico’s duopolist brewers and retailers to the next judicial level. The brewer said in early August 2013 that a Mexican federal court has accepted its case to consider overruling a July antitrust settlement on exclusive sales agreements that SABMiller believes "failed to truly address the monopolistic activities" in the Mexican beer market.

The Americas

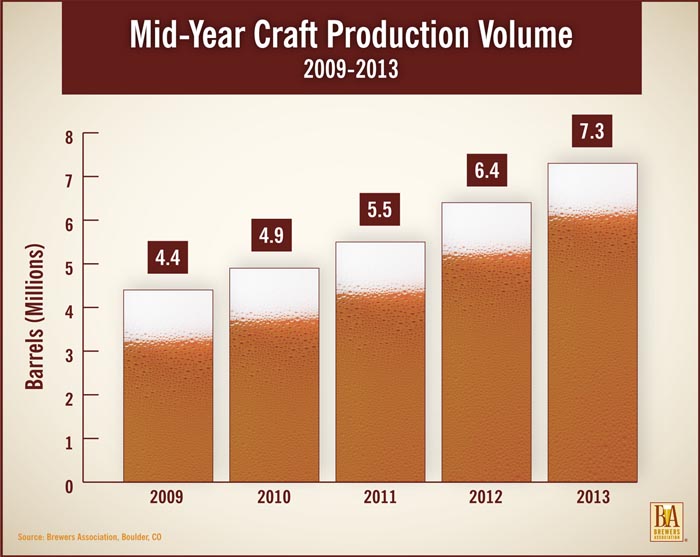

The steady and sustained growth of American craft brewing continued during the first half of 2013, according to mid-year data released by the Brewers Association (BA) at the end of July 2013.

The Americas

Companies beware: No matter how much you shrink the font, some busy-body consumers still manage to read your fine print on labels. Naked Juice Co., a subsidiary of PepsiCo, had to learn this the hard, pecunary way. In July 2013 Naked Juice agreed to a USD 9 million class action settlement over claims it had falsely advertised some of its juices and smoothies as “all natural” and free of genetically modified ingredients.

The Americas

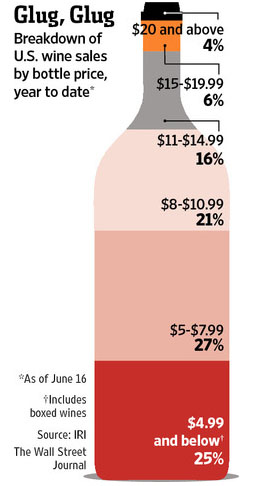

To get rid of excess wine in the U.S., the former Foster’s wine unit Treasury Wine Estates (TWE) said in July 2013 that it plans to destroy AUD 35 million (EUR 25 million) of unsellable wine in the U.S., and to dispose of AUD 40 million worth of lower-quality wine at fire-sale prices in Australia.

The Americas

In her recent book "Sonho Grande" (Big Dream), the Brazilian journalist Cristiane Correa tells the story of entrepreneur Jorge Paulo Lemann, 73, and his two faithful marshals Carlos Alberto "Beto" Sicupira, 65, and Marcel Telles, 63. In little more than four decades, the trio built one of the biggest business empires in the history of Brazilian capitalism and rose to prominence among global investors. Today they are the co-owners of AB-InBev (23 percent of shares), of the fast food chain Burger King and food company Heinz. Together, the three have accumulated a fortune estimated at USD 35 billion, while Mr Lemann himself is often said to be the richest man in Brazil.

The Americas

That’s how SABMiller interpreted the ruling by Mexico’s anti-monopoly agency on 12 July 2013, which basically upholds exclusivity contracts. SABMiller had lodged a complaint with the Mexican antitrust authority in 2010, alleging that the two big brewers – Modelo and FEMSA – lock up much of the market with exclusive contracts. Exclusivity contracts, either verbal or in writing, are where a customer agrees just to sell one brewer’s beer in exchange for financial commitments. Commenting on the resolution, SABMiller said that it did not go far enough to materially change conditions for access and really stoke competition.

The Americas

The steady and sustained growth of American craft brewing continued during the first half of 2013, according to mid-year data released by the Brewers Association (BA). The not-for-profit trade association, which represents the majority of U.S. breweries, announced that during the first six months of 2013, American craft beer dollar sales and volume were up 15 percent and 13 percent, respectively. Over the same period last year, dollar sales jumped 14 percent and volume increased 12 percent.

The Americas

They may be partners with Coors in the U.S., but this did not prevent SABMiller from terminating a licensing agreement with Molson Coors in Canada, to which Molson Coors responded by dragging SABMiller to court.

The Americas

Profit margins in the burgeoning cider segment must be significant or big brewers would not be clamouring to enter this segment. According to media reports in June 2013, Molson, the Canadian arm of brewer Molson Coors, has launched Molson Canadian Cider, following a number of new entrants in Canada, including Labatt’s Alexander Keith’s Original Cider; Brick Brewing’s Seagram Cider; and Carlsberg Canada’s imported Somersby Apple Cider, all of which have already hit stores in 2012.

Most Read

BRAUWELT on tour

Most Read

BRAUWELT on tour

-

Hopsteiner

Hopsteiner breeding program: cutting-edge Technology for yield, resilience, and brewing quality

-

Hopsteiner

Hopsteiner reinforces its sales and marketing teams

-

Hopsteiner

Global acreage, crop and yields

-

Hopsteiner

Global crop estimate 2025

-

Hopsteiner

LLZ™ – hop oil with a pronounced citrus note