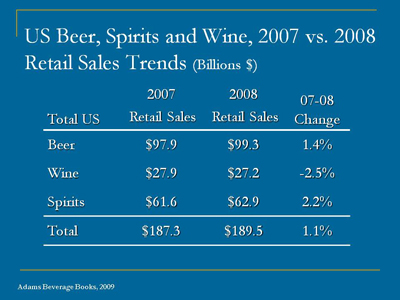

On-premise sales of wine dropped 10 percent in 2009

For the first quarter ended 31 May, Constellation posted earnings of USD 49.1 million, or 22 cents a share, up from USD 6.5 million, or 3 cents a share, a year earlier. Excluding restructuring and other impacts, earnings climbed to 38 cents from 22 cents. Net sales, which exclude excise taxes, dipped 0.5 percent to USD 787.5 million.

Still, the gross margin widened to 34.3 percent from 33.9 percent.

Constellation, which calls itself the global leader in wine but makes the bulk of its revenues in North America, said it grew 5 percent in the first quarter in volumes while the industry grew only 3 percent.

Industry sales in the off-premise sector were up 3 percent during the first quarter. As the off-premise sector only accounts for 70 percent of total sales, Constellation says it needs a strong rebound in the off-premise sector to compensate a stagnating on-premise sector and achieve an annual growth of perhaps 2 percent.

Given that Constellation’s results presentation almost coincided with AB-InBev’s St Louis investor event, which makes a great show of the brewer’s retail strategy, I could not help but notice that the off-premise sector seems to have become such a big thing for these Fast Moving Consumer Goods giants that one would like to shout into their ears: “But the margins are lower than in the on-premise sector and will probably remain so for years to come!”

Although Constellation would never say that it pursues a multi-beverage strategy, despite having spirits brands (Svedka) and international beer brands (Corona Extra) in its portfolio, the challenges it faces resemble very much AB-InBev’s.

True, the on-premise sector in the U.S. and elsewhere remains under pressure because of the economic crisis. Both AB-InBev and Constellation sell a sizeable amount of volume in bars and restaurants. Nevertheless, they want to win at the retail level because retail means scale, transparent execution of promotions, instant results. Certainly it’s not as complex and complicated as the on-premise sector. Especially when dealing with the larger volume players in the U.S. (aka the convenience stores and the supermarkets) AB-InBev and Constellation think they can more easily implement their preferred strategies: big initiatives for a few big brands.

This may be easier said and done for AB-InBev than for Constellation. AB-InBev already dominates the convenience stores and the supermarkets. In beer, the off-premise channel in the U.S. accounts for 80 percent of sales whereas the on-premise accounts for 20 percent. However, it’s a fair guess that most of on-premise sales are controlled by the ubiquitous restaurant chains – hence retail – rather than by individually-owned and managed pubs.

In the wine industry, on-premise sales are higher (reportedly 30 percent) yet wine companies have to deal with a much more fragmented sector than brewers. Especially in the fine dining segment major chains have not made such inroads yet as they have in the casual dining segment.

Like AB-InBev, Constellation announced that from now on it will focus on fewer brands but with bigger retail initiatives. The numbers speak for themselves: Constellation has over 100 brands, except that its top 15 brands bring in 75 percent of its EBIT. In the U.S. Constellation is only the number three player with a 15 percent market share behind E & J Gallo with 26.9 percent and The Wine Group with 21.1 percent (2008) according to the Marin Institute.

Will that lead to a voluntary range rationalisation both at AB-InBev and Constellation? Maybe, but they will always be able to blame it on the retailers.